Futures Market: Overnight, LME copper opened at $9,381/mt, dipping to a low of $9,358/mt shortly after the opening bell. It then fluctuated upward throughout the session, reaching a high of $9,475/mt near the close, and eventually settled at $9,474.5/mt, up 0.73%. Trading volume reached 18,000 lots, while open interest stood at 291,000 lots. Overnight, the most-traded SHFE copper 2506 contract opened at and dipped to a low of 77,540 yuan/mt. It fluctuated rangebound in the early session before rising in the middle of the session, reaching a high of 78,170 yuan/mt near the close, and eventually settled at 78,140 yuan/mt, up 0.72%. Trading volume reached 42,000 lots, while open interest stood at 182,000 lots.

[SMM Copper Morning Meeting Summary] News: (1) US President Trump unveiled a broad framework for a trade agreement with the UK. Speaking from the Oval Office at the White House, Trump said the deal would expand market access for US exports, particularly in agriculture, with greater opportunities for US beef, ethanol, and "almost everything our great farmers produce." Additionally, Trump indicated that the UK would reduce or eliminate several non-tariff barriers.

(2) On the morning of May 8 local time, Russian President Putin held talks with Chinese President Xi Jinping at the Kremlin in Moscow. The two heads of state exchanged in-depth views on China-Russia relations and major international and regional issues, agreeing to unwaveringly deepen strategic coordination and promote the stable, healthy, and high-level development of China-Russia relations. They also jointly advocated for a correct historical perspective on World War II, upholding the authority and status of the United Nations, and safeguarding international fairness and justice.

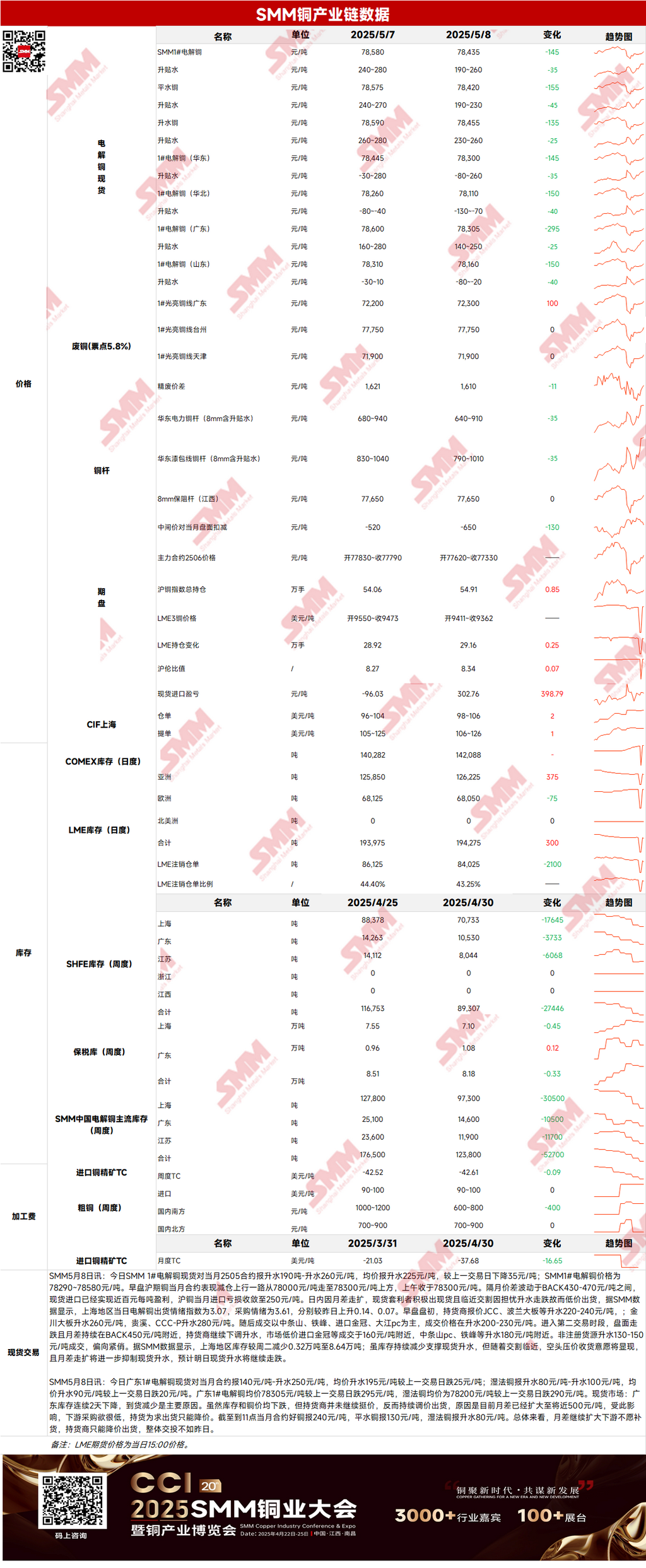

Spot Market: (1) Shanghai: On May 8, SMM #1 copper cathode spot premiums against the front-month 2505 contract were reported at a range of 190-260 yuan/mt, with an average premium of 225 yuan/mt, down 35 yuan/mt WoW. According to SMM data, inventory in the Shanghai region decreased by 3,200 mt from Tuesday to 86,400 mt. Although the continuous decline in inventory supports spot premiums, as the delivery date approaches, bears' willingness to drive down prices and purchase will emerge, and the widening price spread between futures contracts will further suppress spot premiums. It is expected that spot premiums will continue to decline today.

(2) Guangdong: On May 8, Guangdong #1 copper cathode spot premiums against the front-month contract were reported at a range of 140-250 yuan/mt, with an average premium of 195 yuan/mt, down 25 yuan/mt WoW. Overall, as the price spread between futures contracts continues to widen, downstream buyers are reluctant to restock, forcing suppliers to lower prices to sell, resulting in weaker trading activity compared to the previous day.

(3) Imported Copper: On May 8, warrant prices ranged from $98 to $106/mt, with a QP of May, and the average price increased by $2/mt WoW. B/L prices ranged from $106 to $126/mt, with a QP of May, and the average price increased by $1/mt WoW.EQ copper (CIF B/L) is priced between $72/mt and $80/mt, with QP in May. The average price increased by $3/mt MoM. Quotations are based on cargoes expected to arrive in mid-to-late May. Suppliers in the market are actively seeking goods, but offers are limited, driving up premiums.

(4) Secondary copper: On May 8, the price of secondary copper raw materials rose by 100 yuan/mt MoM. The price of bare bright copper in Guangdong was 72,200-72,400 yuan/mt, up 100 yuan/mt from the previous trading day. The price difference between copper cathode and copper scrap was 1,610 yuan/mt, down 11 yuan/mt MoM. The price difference between copper cathode rod and secondary copper rod was 1,425 yuan/mt. According to an SMM survey, due to ongoing losses in the sales of secondary copper rods, some copper rod enterprises plan to suspend production of secondary copper rod lines and switch to producing copper anodes instead.

(5) Inventory: On May 8, LME copper cathode inventory increased by 300 mt to 194,275 mt. On the same day, SHFE warrant inventory decreased by 2,001 mt to 19,540 mt.

Price: On the macro front, Trump announced a trade deal with the UK, raising hopes for similar agreements with other countries. Meanwhile, in the week ending May 3, the number of Americans filing for unemployment benefits for the first time fell by 13,000 to 228,000. After the central bank kept interest rates unchanged on Wednesday, Powell stated that despite potential increases in unemployment and inflation due to tariffs, the labour market remains robust, and copper prices continue to increase slightly. On the fundamental front, from the supply side, as the delivery date approaches, spot arbitrageurs are actively selling due to the widening price spread between futures contracts. However, with the continuous decline in inventory in the Shanghai area, overall supply remains tight, providing some support for spot premiums. From the demand side, although there was some procurement sentiment in the morning, it was mainly driven by just-in-time procurement from some downstream sectors. Overall market activity was average, with no large-scale procurement activities observed. As of May 8, inventory in the Shanghai area decreased by 3,200 mt from Tuesday to 86,400 mt. The continuous decline in inventory supports spot premiums. However, factors such as the widening price spread between futures contracts and the approaching delivery date are expected to suppress spot premiums, which may continue to fall tomorrow. In terms of price, it is expected that there is limited upside potential for copper prices today.

》Click to view SMM Metal Database

[The above information is based on market collection and comprehensive assessment by the SMM research team. The information provided is for reference only. This article does not constitute direct advice for investment research decisions. Clients should make cautious decisions and should not rely on this as a substitute for independent judgment. Any decisions made by clients are unrelated to SMM.]